")

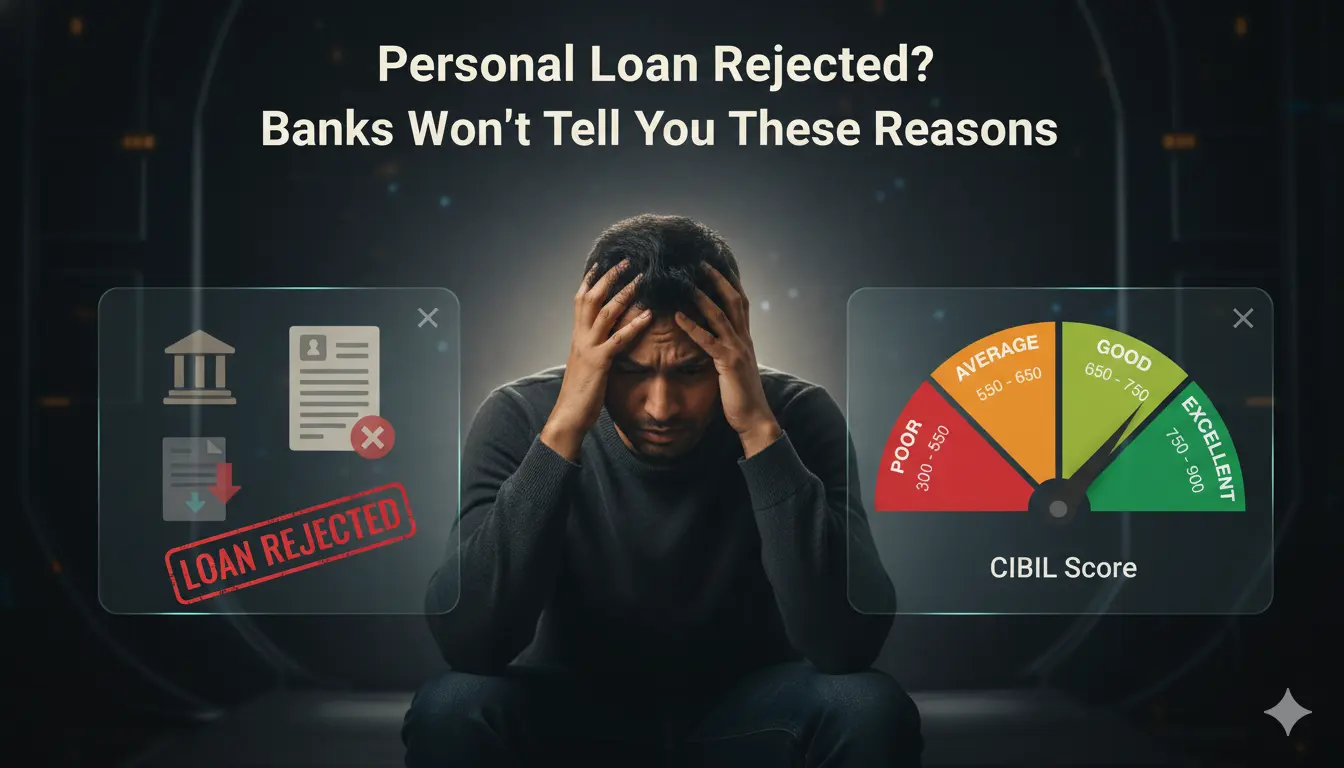

Personal Loan Rejected : You check your CIBIL score. It’s around 700. Your salary is credited on time every month. Still, your personal loan gets rejected—sometimes without a clear explanation. If this has happened to you, you’re not alone. In India, a multiple number of personal loan applications are turned down daily, typically due to reasons that banks rarely clarify. Understanding these obscure factors can assist you in avoiding repeated rejections and improving your chances of approval in the future.

This detailed overview explains the actual personal loan rejection reasons, the impact of these rejections on your credit report, and the steps you can take to resolve the issue.

What Happens If Your Personal Loan Gets Rejected?

When your personal loan application gets denied, it indicates that the lender has chosen not to approve your request after evaluating your overall risk profile. While banks usually give a basic explanation, the real reason is often more complex than simply your credit score.

Immediate consequences of being denied a loan:

- No loan money is disbursed.

- A hard inquiry may appear on your credit report.

You might need to wait before you can apply again.The positive aspect is that a personal loan denial is not forever. In most situations, it does not greatly harm your CIBIL score, especially if you refrain from making multiple applications in a short period.

Table of Contents

Why Loan Rejections Have Increased in 2025?

To comprehend why personal loans were rejected in 2025, it’s crucial to look past individual borrowers and analyze the larger regulatory context that impacts lender decisions.

RBI Tightening Policies on Unsecured Loans

Since late 2023, the Reserve Bank of India (RBI) has tightened policies on unsecured lending to control the rising risks in the retail credit sector.

An important change was the increase in risk weight on personal loans from 100% to 125% for banks and NBFCs.

This leads to an increase in personal loan rejections:

- Banks are required to allocate more capital for each personal loan.

- Creditors consider unsecured lending to be pricier at this time.

- The standards for approval have become stricter.

As a result, borrowers who once qualified with a CIBIL score over 700 may find their personal loan applications rejected in 2025 due to these stricter internal thresholds.

NBFC & Digital Loan App Rejections

The RBI has raised the risk weights on bank loans to NBFCs. Since many digital loan applications rely on bank funding, this has led to:

- A reduction in lending capacity

- Higher rates of personal loan rejections on instant loan apps

- An emphasis on low-risk, high-quality borrowers only

Defensive credit algorithms and job stability risks.

As NPAs in unsecured loans gradually rise, banks have implemented more cautious credit algorithms. Even small warning signs—like a recent late payment, high credit utilization, or employment in an unstable field—can result in a personal loan rejection, even if your income remains stable.

The Hidden Reasons Your Personal Loan Is Rejected

A personal loan is often denied not only because of a low credit score but also due to hidden factors that banks do not explain.

Internal employer rules, a high EMI burden, a thin credit history, multiple recent applications, or even small document errors can quietly cause rejection.

Knowing these hidden causes allows you to address the actual issue and prevent future denials.

Why Your Personal Loan Is Rejected: Employer & Income Risk

A common reason for personal loan rejection is not the amount of your salary but the source of that salary. Banks do not view all employers the same way. The stability, size, and reputation of your employer significantly influence loan approval decisions.

Why Your Company Name Matters in Personal Loan Approval

Banks and NBFCs keep internal lists that classify employers according to their financial stability, history of defaults, and reputation. This internal ranking affects the approval or rejection of your personal loan.

The impact of employer category on personal loan approval:

- Premier employers (PSUs, large multinational corporations, esteemed corporate groups):

- Higher approval rates, reduced income requirements, and better interest rates.

- Mid-sized private companies:

- Moderate scrutiny, increased minimum salary thresholds.

- Small businesses, startups, and unlisted firms:

- High chance of personal loan rejection, even with a good credit score.

- Employers on blacklists or negative lists:

- Automatic denial with no manual review process.

When your employer is classified as lower-risk, it’s easier to get approval—even with a smaller paycheck.

Personal Loan Rejected? Employer Profile May Be the Issue

When you work for a startup, a small private business, or an unlisted company, your likelihood of having a personal loan application rejected rises significantly.

Here’s why:

- Publicly listed companies disclose their financial data; unlisted companies do not.

- Banks find it challenging to determine long-term salary reliability.

- There is a higher chance of business failure or salary delays.

- As a result, banks tend to enforce stricter internal salary limits.

For example, a person earning ₹30,000 at a small startup may be denied a personal loan, while someone earning ₹25,000 at a reputable corporate job might get approved.

This is the reason rejection messages often say “does not meet internal policy criteria”—even when your income and CIBIL score seem acceptable.

Too Many Job Changes? Banks See This as a Red Flag

A solid employer doesn’t guarantee approval for a personal loan if your job history is unstable.

Common rejection triggers related to stability are:

- Changing jobs in the past 6–12 months

- Having less than a year at your current job

- Switching jobs more than 2–3 times in a short period

Being on probation

Banks see frequent job changes as a sign of income instability. Wage hikes don’t always alleviate this risk in credit reviews.

Earning Well but Still Rejected? Your EMIs Could Be the Problem

One major reason personal loans are denied is a high Debt-to-Income (DTI) ratio.

Why banks reject loan applications:

- If your current EMIs are more than 40–50% of your monthly income.

- Having multiple loans or high credit card debt.

For example:If you make ₹40,000 a month and already pay ₹20,000 in EMIs, banks may see you as over-leveraged—even with a credit score of 750.

How to improve your chances:

- Pay off small or high-interest loans.

- Cut down on credit card debt.

Key Takeaway

A decision to reject a personal loan is usually based on employer risk, job stability, and current debts—not only your credit score. Knowing these unseen factors can help you apply at the right time and prevent getting rejected again.

Why a Thin Credit History Can Get Your Loan Rejected?

A credit score of 700 doesn’t guarantee a strong profile. Often, personal loans are denied due to a thin or inactive credit history.

Reasons banks are concerned:

- Few active loans or credit cards

- No recent credit activity

- Long periods of inactivity

Banks favor borrowers who show a clear repayment history, rather than just a score.

Steps to take:

- Use a credit card consistently

- Pay your bills on time.

- Keep activity going for at least 3 to 6 months

Multiple Loan Applications in a Short Time

Applying to multiple banks or instant loan apps at once is one of the fastest ways to face rejection for your personal loan.

Every application generates a hard inquiry on your credit report, and when lenders observe several inquiries in a short span, it suggests financial distress or an urgent need for credit.

Consequently, banks are often more cautious, even if your credit score is within an acceptable range.

As a rule of thumb, it is beneficial to wait 30–90 days between loan applications to decrease the likelihood of receiving multiple rejections.

Internal Bank Rules You’ll Never Be Told

It is common for personal loans to be denied because of internal bank policies that are not revealed to customers.

Each bank utilizes its own hidden criteria—such as city tier or pin-code eligibility, age limits (particularly for self-employed applicants), and minimum income stability standards. As these criteria vary from one lender to another, it is typical to find one bank rejecting your application while another grants approval immediately, even with the same paperwork and credit score.

Small Document Errors That Cause Big Rejections

At times, a personal loan may be denied due to minor issues such as discrepancies in data or documents. Problems like a PAN–Aadhaar mismatch, variations in the spelling of your name, salary slips that do not align with bank statements, or incorrect employer information can lead to automatic rejection during the verification process. Given that these mistakes are often easy to miss yet can be expensive, it is crucial to thoroughly review all documents and details prior to submitting a loan application.

Low or Recently Damaged Credit Score

Even at present, the vast majority of banks prefer borrowers who have a CIBIL score of 700 or more, and falling short of this range often leads to the rejection of personal loan requests. Usually, a score of 750 or above provides a strong likelihood of approval, while scores between 650 and 749 are in a conditional area where other risk elements are scrutinized. Scores below 600 are considered to carry a high rejection risk. Moreover, a recent late payment or a ‘settled’ account can diminish an otherwise satisfactory credit score and cause rejection.

Frequently Asked Questions About Personal Loan Rejection

Does Personal Loan Rejection Affect CIBIL Score?

A personal loan rejection doesn’t directly lower your CIBIL score. However, applying to multiple lenders in a short time can hurt your score due to repeated hard inquiries. One rejection has minimal impact—avoid reapplying until you fix the reason for denial.

How long should I wait after loan rejection?

It is best to wait 30 to 90 days before you apply again. Use this time to address the reasons for your rejection—such as high EMIs, problems with documentation, or low credit activity—so that your next application has a higher probability of success.

Can I get a personal loan with 550 CIBIL score?

Receiving a personal loan with a 550 CIBIL score is difficult through banks. Some NBFCs or fintech lenders may allow it, but typically at higher interest rates and more demanding conditions.

Why is my credit score 700 but still rejected?

A score of 700 doesn’t guarantee approval. High EMIs, employer risk, thin credit history, recent job changes, internal bank rules, or document mismatches are common reasons for rejection.

What is the minimum CIBIL score for a personal loan?

Most banks prefer a minimum CIBIL score of 700, while scores between 650–699 may get conditional approval depending on income and other factors.

Can a Loan Be Approved After Rejection?

Yes, a loan can still be approved after a personal loan rejected decision. Many borrowers get approved within 1–3 months by reducing their EMI burden, fixing document or data issues, and applying to a lender that better matches their profile. In most cases, strategy matters more than urgency.

What to Do If You Need Money After Loan Rejection

In the event that your personal loan is denied, do not hurry into another application. Consider the option of reducing the loan amount, adding a co-applicant, or exploring NBFCs that have more flexible eligibility requirements. Secured loans, like those backed by fixed deposits, are typically safer and more economical. Refrain from using high-interest instant loan apps unless absolutely required.

How to Improve Your Personal Loan Approval Chances

Improving your approval chances can be done by keeping your EMIs at or below 40% of your income, ensuring credit utilization is under 30%, avoiding frequent job changes, and applying only to lenders where you are eligible.

Final Takeaway

Personal loan turned down. The bulk of rejections result from issues that can be remedied, yet banks do not consistently offer clear insights. By grasping the actual reasons and fixing them before you submit another application, your odds of being approved increase substantially.

Enable push notifications to get real-time updates on loan eligibility advice, approval strategies, and changes in banking regulations—ensuring you are thoroughly prepared for your upcoming loan application and can avoid unnecessary denials.