Three digits make up your CIBIL score, a “report card” of your financial behavior. They utilize it to determine whether or not you are eligible for a loan. Young Indians (students, professionals, and entrepreneurs) who have aspirations of establishing a company or purchasing a house or automobile might benefit from having a favorable CIBIL score since it enables them to get credit cards and loans with cheap interest rates. In fact, well over 119 million Indians monitored their CIBIL scores in the fiscal year 24 (FY24), which is a 51% increase from the previous year. This data demonstrates the rising awareness of credit, particularly among members of Generation Z and millennials. Therefore, what is a decent score on the CIBIL? What is considered a “good” score, and what are some ways that you may help raise your CIBIL score quickly? The language used in this tutorial is easy to understand and suitable for beginners. It also includes helpful hints and analogies that are appropriate for the Indian setting.

What is a CIBIL Score and Why It Matters

The Credit Information Bureau of India Ltd. (CIBIL) is responsible for keeping track of your credit history, which includes payments on loans, credit cards, and bills, and assigning a score ranging from 900 to 900. “It” informs banks how responsible you are with money, so you may think of it as your financial report card or as a “digital credit handshake.”

It is preferable to ascend. A bad CIBIL score can make it harder to get loans or credit cards and raise interest rates. If, on the other hand, you have a high score, lenders will have greater faith in you, which will result in easier access to loans at more favorable interest rates.

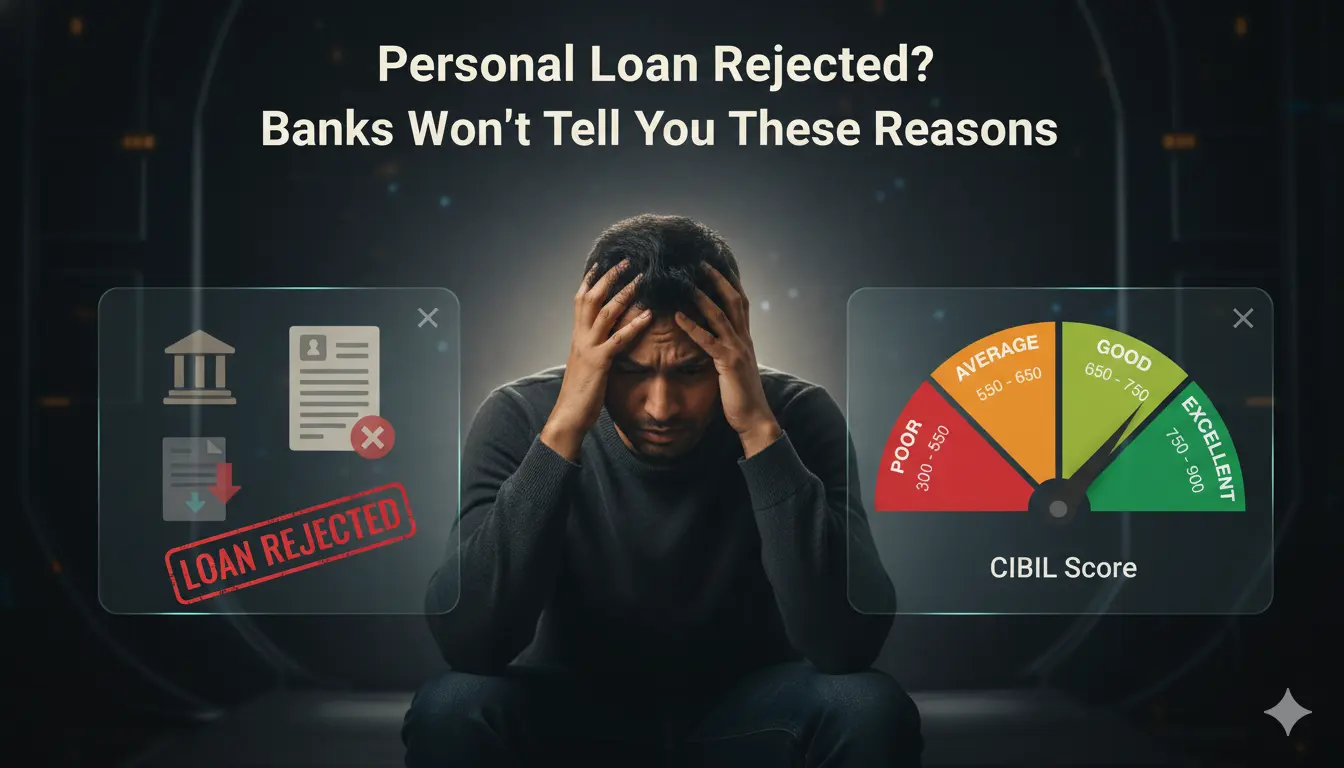

The range of possible scores on the CIBIL is as follows: Poor (300–550), Fair (550–650), Good (650–750), and Excellent (750–900). To be in the “good” zone, you should strive to get a score of 700 or above. A score of 685 or above, according to Bajaj Finserv, considerably boosts the likelihood of obtaining a loan approval on conditions that are acceptable.

Why it is significant: Forbes India refers to your credit score as a “financial passport” that provides access to options like house loans, auto loans, and even luxury apartment rentals. To put it another way, having a respectable CIBIL score may expedite the approval process and save you millions of rupees in interest.

Your CIBIL score shows how well you handle your money, such paying your bills on time, keeping track of your debt, and other similar things. Because you have developed excellent financial habits, you will be able to save more money in PF, FDs, or SIPs now, rather than paying more interest on loans in the future.

Table of Contents

How to Check Your CIBIL Score Online

Before you try to improve your score, be sure you know where you stand right now. Online CIBIL score checks are a breeze, which is a fortunate development:

Visit the official website of TransUnion CIBIL to get your credit score. You may do this by checking out the website. Every individual receives free credit reports annually, as required by law. Just sign up with your PAN, name, and date of birth, and you’ll receive your score and report. Some banks and financial apps offer your CIBIL score for free or include it as part of their services, making it easier for you to check it more often.

India has four credit bureaus: CIBIL, Equifax, Experian, and CRIF High Mark. CIBIL is the most frequently utilized. Additionally, you have the option to obtain reports for free or for a fee from other sources. However, a single free TransUnion CIBIL report is typically sufficient.

Credit monitoring applications and websites, such as Paisabazaar, BankBazaar, Paytm, and others, enable you to view your CIBIL score, typically following a sign-up process. Free score updates may be offered periodically. Make sure to utilize a secure and authorized website.

Why do routine checks? Examining your credit report enables you to identify errors. Errors (such as a misplaced loan or incorrect personal information) might lower your score. Find any errors and dispute them with the agency as soon as possible.

Pro tip: Check out your CIBIL score constantly, particularly before big loans. New RBI guidelines update your score every 15 days; therefore, favorable changes—like loan clearance—show up sooner.

What is a Good CIBIL Score?

A common question is, “What CIBIL score is considered excellent in India?” In general:

700+ – Satisfactory. Securing loan approvals will be straightforward, and you can expect lower interest rates.

750–900—Outstanding. You are probably going to secure the most favorable loan offers. According to TransUnion and industry experts, a score of 750 and above is considered ideal.

650–699 —acceptable to Satisfactory. Loans are frequently available, though the interest rates might not be the most competitive. Strive to elevate this further.

A score of less than 650 is considered below average. Lenders may be hesitant to provide loans or could charge higher interest rates.

Remember: thresholds vary by lender. Bajaj Finserv notes even 685+ is a strong score that boosts approval odds. But aim for 700+ to stay on the safe side.

Quick Tips to Improve Your CIBIL Score Fast

There is no secret formula for improving your CIBIL score; nonetheless, developing good practices may help it increase slowly. Here are several proven methods that can be implemented within a few months, especially considering the increasing frequency of data updates:

Always ensure bills are paid promptly and consistently. This is the most significant factor. Paying your EMIs, credit card bills, and utility bills on time demonstrates your ability to manage debt effectively. Consider every due date as a homework deadline—if you miss it or pay late, your score will decrease. Establish reminders or automatic payments to ensure everything is on time.

Maintain a minimal level of credit consumption. This indicates that you should avoid using your credit card to its maximum limit. In an ideal scenario, you should use no more than thirty percent of the maximum on any card. For instance, if you have a limit of ₹50,000, you should not retain more than ₹15,000 in your account balance. You may even contact your card issuer to boost your credit limit if you don’t use it very often. Your usage ratio will decrease if you take advantage of a greater limit while maintaining the same level of expenditure.

Try not to apply for too many loans or credit cards at once. Whenever a lender examines your credit, it may cause a slight drop in your score. Applying for multiple loans or credit cards in a short time can give off the impression that you’re under financial stress. Please take your time when completing the applications. Make sure to apply only when you truly need credit.

It is important to maintain those previous accounts. I just wanted to give you a heads-up: when you have paid off your previous loans or credit cards, you should strive to avoid closing them immediately. It’s something that should be considered first! It is unquestionably advantageous to have a longer credit history. If you have an old account that has a favorable track record, it is comparable to having a senior in school who is respected; it provides a significant boost to your reputation. It is a clear indication of your level of responsibility if you are able to pay off a vehicle loan. Rather than canceling that account, it might be preferable to leave it “open” if you can do so.

Maintain a balanced credit portfolio. A combination of several sorts of credit, such as a credit card, a personal loan, and a “one-day” house loan, is a good thing. It demonstrates that you are capable of managing a variety of loans. However, do not take out debts that you do not need merely for the sake of mixing. It is better to have one small loan and a credit card that you pay off promptly than to have many unnecessary loans.

Reduce the amount of existing balances. Please make every effort to pay off your substantial credit card balances as quickly as possible. By reducing your usage and demonstrating that you have a solid habit, paying down your main debt may help improve your credit score. Attempt to pay off the card with the highest interest rate first.

Your credit report should be checked and corrected. Get a copy of your whole credit report and carefully examine it. You should immediately file a dispute if you discover any incorrect accounts or if a loan that has been paid in full is still displaying as delinquent. There are situations when correcting mistakes might offer your score a substantial boost.

Consider making your EMI payments more frequently. Consider making your EMI payments every six months or even quarterly, if you can, rather than adhering to a monthly schedule. Lenders update your outstanding balance every 15 days, so if you pay earlier in the cycle, it can show a lower outstanding amount. Such an arrangement might give a slight boost to your utilization and repayment history.

Consider going for longer loan terms. If you go for a longer loan tenure, your EMIs will be smaller, making it less likely for you to miss a payment. If you’re finding those big EMIs tough to handle, Bajaj Finserv suggests that opting for a longer term can help keep your payments manageable and prevent defaults, which can gradually improve your score.

Consider the process of enhancing CIBIL to be more of a habit game than a one-time hack. Maintaining consistency over a period of months (usually between four and twelve months) can steadily enhance your score. The RBI’s new reporting requirement has accelerated the recording of your positive activities.

Common Mistakes to Avoid

You haven’t made even a single payment. This is a massive red mark.

You’re closing your old cards too quickly. This action abruptly reduces the length of your credit history.

You should limit your payments to the lowest possible amount. If possible, please try to pay off your credit cards in full each month.

Don’t overlook smaller debts. Loan defaults of any size are detrimental.

You are not treating the role of a co-signer with seriousness. The default of a loan that you guaranteed will have a negative impact on your credit score.

You’ll see consistent progress if you steer clear of them and follow the advice given above.

Frequently Asked Questions (FAQs)

What is a CIBIL score?

Your CIBIL score is a 3-digit number, ranging from 300 to 900, that shows how trustworthy you are when it comes to credit. Your credit history, including your loan repayments, credit card usage, and other borrowings, determines your CIBIL score. TransUnion CIBIL, one of the top credit bureaus in India, A higher credit score increases your chances of loan approval and lower interest rates.

What is a good CIBIL score

A solid CIBIL score often runs from 700 to 900. This range indicates that you’ve got a solid credit history and are managing your finances well. Most banks and lenders usually look for a score of 750 or above when it comes to approving credit cards or loans.

How much CIBIL score is good for a loan?

In India, a CIBIL score of 700 or more is regarded as satisfactory for the majority of loans. On the other hand, a score of 750 or above is desirable since it allows for speedier approvals and cheaper interest rates. It is possible that certain lenders may accept loans with scores ranging from 650 to 699; however, the interest rates may be higher.

How to check cibil score free

At the official website of TransUnion CIBIL, you are able to check your CIBIL score online for free once per year. Simply provide your name, the number on your PAN card, and your contact information when you join up. Numerous applications, such as Paisabazaar and BankBazaar, as well as some banking applications, such as Paytm and PhonePe, provide free CIBIL score checks after the login or registration process.

Is credit score and CIBIL score the same?

Absolutely, but also not quite. A CIBIL score represents a specific category of credit scores. India boasts four primary credit bureaus: CIBIL, Equifax, Experian, and CRIF High Mark. While various options provide a credit score, the majority of Indian lenders specifically rely on the CIBIL score. While every CIBIL score qualifies as a credit score, not every credit score originates from CIBIL.

Conclusion

Your CIBIL score plays a crucial role in building your wealth. It helps you borrow smartly, save on interest, and gives you more money to invest in things like SIPs or FDs. Would you consider starting by checking your CIBIL score online today and reviewing your report? So, go ahead and put these tips into action: make sure to pay everything on time, keep your credit usage low, and focus on building those healthy credit habits. Just keep in mind, staying consistent is the key.

The creator of Eco Nivesh, Mohammad Faijan (Faizaan Raza), has a degree in commerce. To assist young Indians in making secure, knowledgeable financial decisions, he writes about personal finance, insurance, taxes, and digital money techniques.

")